Bio

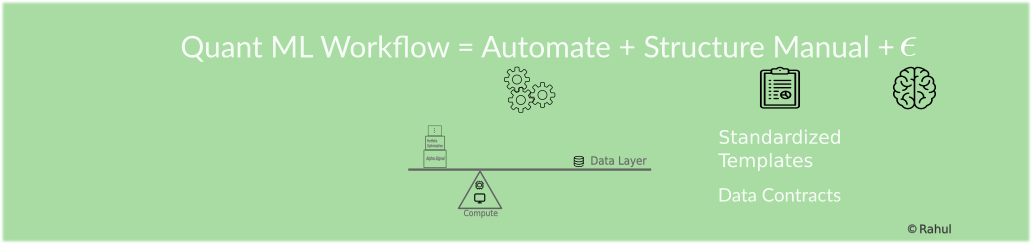

I am an applied mathematician working at the intersection of mathematics, AI/ML, and quantitative investment strategy. I hold a PhD in Applied Mathematics and Certificate in University Teaching from the University of Waterloo, Canada. I am a systems thinker—leveraging interdisciplinary skill sets to identify factors that generate returns over time and designing efficient, repeatable processes. To build interpretable and robust investment strategies, I follow the framework (Figure 1), which decomposes processes into three key components (Equation 1):

Automation – Streamlining tasks that can be fully systematized.

Structuring the Manual – Organizing and optimizing the elements that still require human input or still not available via databases through:

Domain Expertise – Developing deep knowledge to manage uncertainty and handle the unknown.

Formally, this framework can be expressed as following workflow:

\[ \text{Quant ML Workflow = Automation + Structure the Manual + } \epsilon \tag{1}\]

Where \(\epsilon\) represents the unknown component, requiring domain expertise to ensure process resilience, particularly during Black Swan events such as COVID-19.

Professional

I am currently a Lead Quantitative Modeler at Finance in Motion GmBH, Frankfurt, Germany. My work sits at the intersection of technology, investment factors, risk management, and mathematics, where I:

Develop and implement systematic investment signals/insights using quantitative methods to:

Rebalance portfolio exposures to maximize yield while ensuring compliance with fund investor protection limits and the risk profile.

Optimize portfolio composition for new fund construction.

Manage FX risk and CreditMetrics based portfolio risk models.

Develop and manage the technology infrastructure for both model development and production model deployment using MLOps principles, ensuring scalability, reliability, and automation throughout the model life-cycle. Key infrastructure include:

Moody’s CAP (AWS + MLflow) infrastructure

Azure Virtual Machines